You send someone a card. The money is on it. They try to buy something online, and it gets declined. Nothing is wrong with the balance. What is missing is proof of who the card belongs to. Before a merchant approves an online payment, it runs a few quiet checks on exactly that, and a card without the right details on file fails them. Here is how those checks work, and why the details you register matter more than the balance you load.

A card is more than a number

Behind every card is a set of registered details: the cardholder's name and a billing address held by the issuer. In person, those rarely come up. Online, they are the whole game. A card-not-present purchase has no physical card and no signature, so the merchant leans on the registered details to decide whether the person paying is really the cardholder.

What AVS checks

The first check is the Address Verification System, or AVS. The merchant takes the billing address entered at checkout and asks the card network to compare its numeric parts, the street number and the ZIP, to the address on file for that card. A clean match comes back as a full-match code. No address on file comes back as unavailable. To a merchant deciding whether to take the risk, "unavailable" reads a lot like "cannot be trusted."

The name behind the card

Most merchants now add a second check: the cardholder name, comparing what is entered at checkout to the name registered on the card. A card issued without a real name has nothing to match, which is one more reason to decline. Stack an unverifiable address on top of a missing name, and to an automated fraud system the transaction looks indistinguishable from a stolen card.

Why any address won't do

There is a subtler trap. Some programs do put an address on their cards, but they use the same one for every card they issue. That solves the "no address" problem and creates a worse one. When hundreds of cards transact from a single billing address, fraud systems see a cluster and start flagging, throttling, or blocking, and many merchants cap how many orders can come from one address. So a real, unique address per card is not a nicety. It is what keeps each card looking like a separate, legitimate person instead of part of a pattern.

What missing details cost you

Every one of these failures lands on the sender. A declined reward is a recipient who feels let down and a ticket for your support team. A payout that will not spend is not a payout. For a program built to create goodwill, a card that dies at checkout does the opposite. The cards that work are the ones whose details are registered properly: a real name, and a real, unique address.

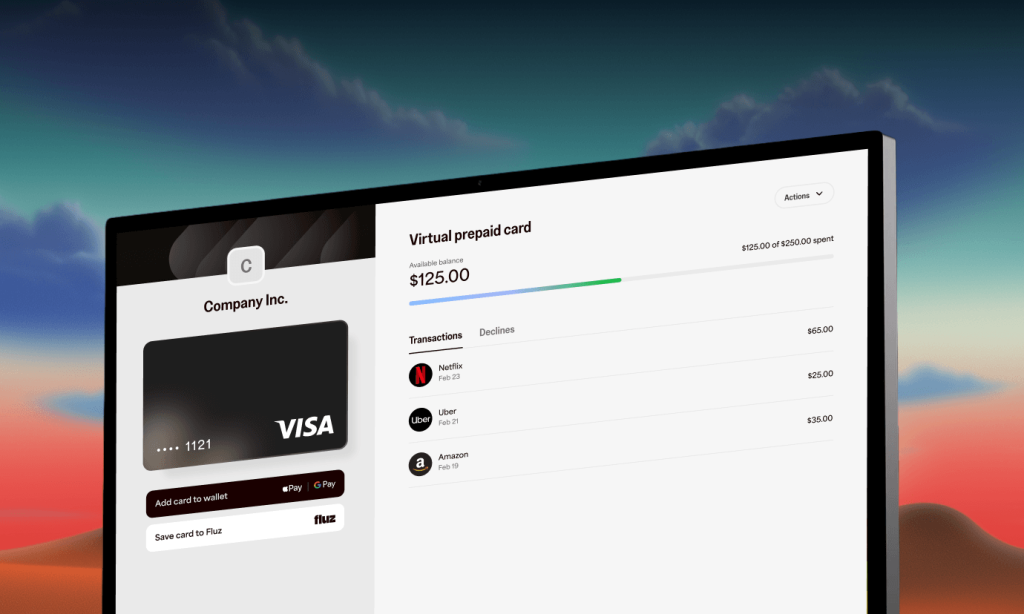

How Fluz clears every time

Now put the two side by side. Every failure in this article traces back to a missing or shared detail, and that is the one thing Fluz refuses to leave to chance. Every Fluz card is registered to the real recipient and carries its own unique billing address. AVS returns a full match. The name check passes. The card behaves like a personal card the merchant already trusts. No "unavailable" codes, no shared-address clusters, no cards blocked before checkout even loads.

The table below is the short version. The longer version is the outcome you wanted when you sent the reward in the first place: it spends. Recipients use their cards instead of opening tickets, your payouts land as goodwill instead of frustration, and your program grows without dragging a trail of declines behind it.

Why registered cards clear

| Fluz | Typical anonymous reward / prepaid cards | |

|---|---|---|

| Cardholder name | Registered to the recipient | None |

| Billing address | Unique, registered per recipient | None or shared placeholder |

| AVS result | Full match | Unavailable |

| Name match | Passes | Nothing to match |

| At checkout | Clears like a personal card | Often declined |

| Anonymous-card blocks | Avoided | Frequently blocked |

| Recipient experience | Spends anywhere | Declines and support tickets |

Stop sending cards that fail at the register. Send cards that clear the first time. Talk to an expert or open an account.

'%3e%3cpath%20d='M274.28%20122.898V243.353L211.796%20230.331V577.862H36.5165V230.331H0V122.898H35.7051C35.7051%2030.9281%20103.058%200.000301701%20189.886%200.000301701C217.945%20-0.0330143%20245.94%202.69299%20273.469%208.13919V88.7142C261.668%2086.7113%20249.731%2085.6228%20237.764%2085.4586C210.173%2085.4586%20193.132%2095.2253%20193.132%20122.898H274.28Z'%20fill='%23170100'/%3e%3cpath%20d='M302.648%208.13672H477.928V577.859H302.648V8.13672Z'%20fill='%23170100'/%3e%3cpath%20d='M781.416%20118.012H957.507V577.859H782.228L824.424%20354.04H812.252C781.416%20541.234%20740.031%20585.998%20650.768%20585.998C564.751%20585.998%20509.57%20534.723%20509.57%20419.965V118.012H685.661V340.203C685.661%20388.223%20699.457%20411.012%20731.916%20411.012C765.186%20411.012%20781.416%20385.781%20781.416%20325.553V118.012Z'%20fill='%23170100'/%3e%3cpath%20d='M1359.99%20412.64V577.859H991.581C985.901%20557.512%20981.844%20520.073%20981.844%20492.401C981.844%20428.917%201015.11%20376.828%201072.73%20333.692C1110.06%20305.206%201164.43%20274.278%201213.93%20252.303L1213.12%20243.351C1153.07%20265.326%201051.63%20281.603%20986.713%20281.603V118.012H1357.56V285.673C1251.26%20346.714%201174.16%20399.617%201136.02%20467.17H1147.39C1185.53%20424.034%201238.27%20406.128%201293.45%20406.128C1315.79%20406.077%201338.08%20408.259%201359.99%20412.64Z'%20fill='%23170100'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_4352_6280'%3e%3crect%20width='1360'%20height='586'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)